Fixing Your Credit Score

January 10, 2023

To start improving your credit score, it helps to know what goes into making it. The factors that affect your score are:

- Timely payments: 35%

- Overall debt: 30%

- Length of credit: 15%

- New credit applications: 10%

- Types of credit: 10%

Know Your Score

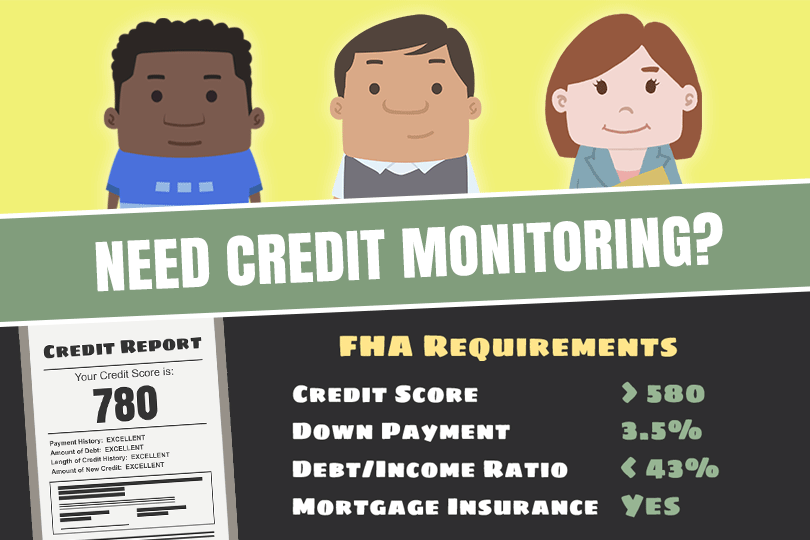

You need to know what your score is if you want to get started on improving it for a home loan. According to the Fair Credit Reporting Act, individuals have the right to their own credit report, which is available from a credit bureau. You can request your report from these bureaus, the top three of which are Equifax, TransUnion, and Experian. Once you have your report, you can review it and dispute any discrepancies. The bureaus are responsible for investigating any disputes within 30 days.

Don’t Let Your Balance Go Past-Due

The most important factor that makes up your credit score is your payment history. 35% of your credit report depends on whether or not you make payments on time. The later you are on those payments, the worse it is for your credit report. Always try to pay off your credit balances in full. Not only does this keep you from incurring large interest payments, but having a “paid in full” remark on your credit report looks good to lenders considering you for a loan.

Building a Credit History from Scratch

Many first-time homebuyers run into the problem of not having a sufficient credit history. This can affect the 15% of your score that depends on age of credit. Establishing credit history can start with signing up for a credit card and using it to pay for everyday items. It also helps to set up utility payments through your credit card online. Just remember to pay off the balance on time!

Be Proactive About Opening New Lines of Credit

When applying for a loan or credit card, your bank or lender performs a “hard inquiry.” This is a review of your credit that in turn affects your score. If you submit multiple credit applications in a short timeframe, it shows up as a red flag for lenders. They might assume that you aren’t handling your finances well enough if you need multiple lines of credit open at once. It’s important that you don’t submit credit applications close to the time that you apply for a home loan.

Remember that your credit score represents your creditworthiness. Based on this number, a lender determines whether you are a high-risk borrower and if it’s a smart idea to loan you a huge amount of money. It also determines the interest rate you’ll receive from the lender, so it is worth your time to work on increasing your score.

------------------------------

RELATED VIDEOS:

Learn How to Meet FHA Requirements

A Few Tips About Your Fixed Rate Mortgage

Your Proof of Ownership Is the Property Title

FHA Loan Articles

April 16, 2025There are smart uses for cash-out refinancing loan proceeds and uses for that money that may work against the borrower. We examine some of those choices below, starting with using an FHA cash-out refinance for investment purposes. Is this a good idea?

April 15, 2025House hunters sometimes face a curveball when the appraisal for a home they want to buy with an FHA mortgage is lower than the offer. Is this a deal-breaker? Believe it or not, it isn't the end of the road. A low appraisal can sometimes be just a bump in the road. In other cases, you may wish to walk away from the deal. Here's your game plan to navigate this situation...

April 14, 2025 Buying a home with an FHA loan can be an exciting and achievable goal. This quick quiz helps you gauge your understanding of FHA loans and what it takes to make a winning offer on your new dream home. Take a few moments to answer the questions and see how prepared you are to navigate this crucial stage of your home-buying journey.

March 31, 2025Is 2025 the right year for you to consider an FHA streamline refinance? These mortgages are for those who want a lower interest rate, a lower monthly payment, or to move out of an adjustable-rate mortgage and into a fixed-rate loan. We examine some of the critical features of FHA streamline refinances.

March 27, 2025Did you know there are FHA loans that let house hunters buy multi-family properties such as duplexes and triplexes? FHA rules for these transactions is found in HUD 4000.1, including owner-occupancy, require that one unit serve as the borrower’s primary residence. Some house hunters ask why this rule exists. Some believe the rule serves as a lender risk mitigation strategy.