Beyond the Break-Even With FHA Discount Points

April 30, 2025

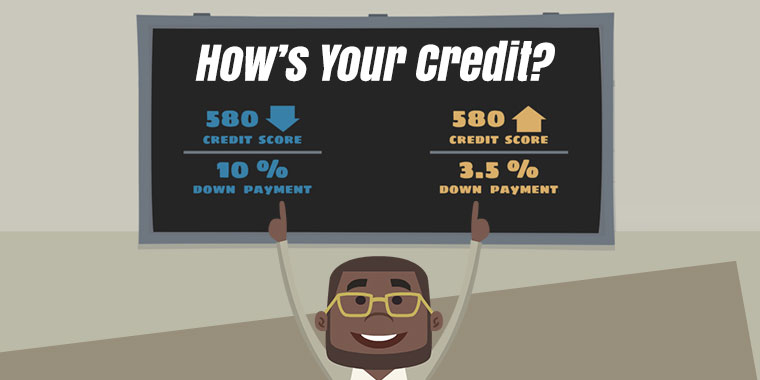

Discount points are an option for borrowers willing to pay a fee to lower the interest rate by a set amount. This is not right for all borrowers, and you don't want to pay for points you won't benefit from during the loan term.

That's why it pays to ask some critical questions. Are you a first-time homebuyer feeling overwhelmed by the process? Do you anticipate changes in financial or housing needs in the coming years?

The discount point question can be complicated. Calculating break-even points, projecting long-term savings, and weighing the opportunity cost of your capital is time-consuming and requires dedication.

For some FHA borrowers, accepting the lender's offered interest rate without the added layer of points can simplify the transaction. Doing so lowers the risk of making a decision they don't fully grasp or later regret. Sometimes, keeping things simple is best, but not always.

An important factor when weighing your discount points options is the possibility of refinancing your FHA loan in the future.

Interest rates are subject to market shifts. If rates experience a significant downturn, you might be able to refinance your FHA loan at a more favorable rate. If you've already paid for discount points on your original loan, the financial benefit of that upfront investment could be entirely negated by a future refinance.

If you think you may refinance in the coming years, paying for discount points now introduces the risk of that cost becoming a "sunk expense." Not all borrowers fully comprehend the mechanics of how points work and the extended timeframe often required to recoup their cost.

While lenders are responsible for clearly explaining the costs and potential savings, it's equally your responsibility to ask questions and ensure you thoroughly understand the implications.

Discount points are best for those who plan to keep the home and the original mortgage long-term. If that doesn't sound like you, avoiding paying for discount points may be best.

Remember, the goal is not just to get approved for the FHA loan, but to secure a loan that serves your long-term financial needs. Weigh the cost of buying points against the uncertain future benefits of doing so. Make your financial health the priority.

FHA Loan Articles

December 10, 2024The FHA announced increased loan limits for 2025, providing those seeking FHA-insured mortgages after January 1st with increased purchasing power. In this article, we explore the key aspects of these limits and their implications for your homeownership goals.

When you are approved for an FHA-insured loan, the FHA guarantees a portion of the loan to the lender, lowering lender risk...

December 9, 2024The Federal Housing Administration (FHA) helps people buy homes, especially those buying for the first time or who might not have perfect credit. In 2025, there is good news for FHA borrowers. FHA home loan limits are going up.

In most places, the FHA loan limit for a single-family home in 2025 is $524,225. This is more than it was in 2024. However, in expensive areas, where houses cost more, the limit can be as high as $1,209,750.

December 5, 2024The Federal Housing Administration (FHA) has some ground rules regarding cash-out refinances. These rules are designed to protect both you and the lender, ensuring you have enough ownership of your home and reducing the risk of foreclosure. How long must you own your home before you can apply for FHA cash-out refinancing?

December 4, 2024When you think about owning a farm, do you dream of vast landscapes and thriving agricultural enterprises? Or are you looking for a quaint farm-style house to live in but not necessarily to start a new farming career?

Borrowers who want to buy a farm residence are in luck with the FHA loan program, which includes options to purchase farm residences.

November 27, 2024If you are new to the home loan process, you may wonder how your loan officer will interpret your application data. How lenient is the lender with issues related to debt, credit utilization, and related factors? We examine some key points, but remember that what follows is not financial advice. Always consult a finance or tax professional for the most current information.