Understanding FHA Loan Debt Ratios

July 29, 2023

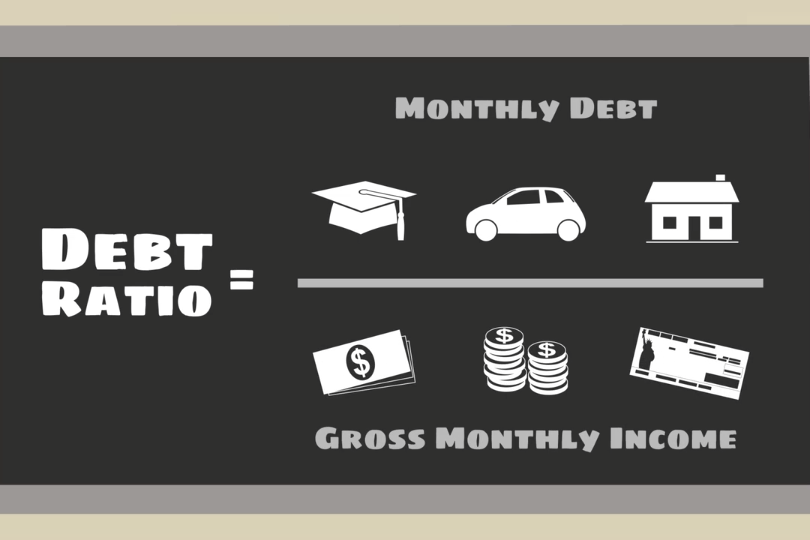

FHA loan debt ratios are financial benchmarks that assess a borrower's ability to manage their debt and make mortgage payments on time. These ratios play a pivotal role in the FHA loan approval process, as they provide a snapshot of a borrower's financial health. Two primary debt ratios are considered when evaluating an applicant's eligibility for an FHA loan:

Front-End Ratio (Housing Ratio)

This measures the percentage of a borrower's monthly gross income that will be allocated to housing-related expenses. These expenses include mortgage principal and interest, property taxes, homeowners insurance, and mortgage insurance premiums (if applicable). FHA guidelines typically require that the housing ratio does not exceed 31% of the borrower's gross income.

Back-End Ratio (Total Debt Ratio)

This is a broader measure of a borrower's debt load. It considers not only housing-related expenses but also other monthly obligations such as car loans, credit card payments, student loans, and any other outstanding debts. The FHA generally sets a maximum allowable back-end ratio of 43% of the borrower's gross income.

To improve your back-end ratio, focus on paying down existing debts, such as credit cards and personal loans. Reducing your overall debt load can make you a more attractive candidate for an FHA loan.

Both of these ratios serve as vital tools for lenders to assess your financial health and determine your eligibility for financing. By managing your debt wisely, increasing your income, and budgeting carefully, you can improve your debt ratios and increase your chances of securing an FHA loan. Remember that while debt ratios are an essential part of the approval process, they are just one piece of the puzzle, and other factors like credit score and down payment also play a role in determining your loan eligibility.

------------------------------

RELATED VIDEOS:

Let's Talk About Home Equity

Understanding Your Loan Term

Your Home Loan is Called a Mortgage

FHA Loan Articles

April 30, 2025 In a previous post, we discussed why FHA borrowers should carefully consider whether paying for discount points truly serves their best interests, focusing on factors like short-term homeownership, opportunity cost, FHA mortgage insurance, and the prevailing interest rate environment. Discount points are an option for borrowers willing to pay a fee to lower the interest rate by a set amount. This is not right for all borrowers, and you don't want to pay for points you won't benefit from during the loan term.

April 29, 2025Are you considering buying a home with an FHA loan? You'll likely talk to your participating lender about FHA loan "discount points" – fees you pay upfront for a lower interest rate on your mortgage. The idea behind discount points is a straightforward exchange: you spend money today to reduce your interest rate. Typically, one point equals one percent of your total FHA loan. In return, your interest rate might decrease by an amount you and the lender agree upon.

April 28, 2025Home loans have various expenses that aren't apparent to a new borrower until much later in the process. What do you need to consider when making your home loan budget? It might not be complete without addressing some of the issues we cover here.

April 23, 2025 While the prospect of lower interest rates or more favorable loan terms can be enticing, there are situations where waiting is the better option. Refinancing without carefully considering your current financial circumstances is never a good idea, but careful planning in the current financial environment is even more important.

April 22, 2025First-time home buyers worry about loan approval, but there are important steps to take to increase the likelihood that the lender will approve their application for the loan or pre-approval. What do you need to know before you choose a lender?