Understanding FHA Loan Debt Ratios

July 29, 2023

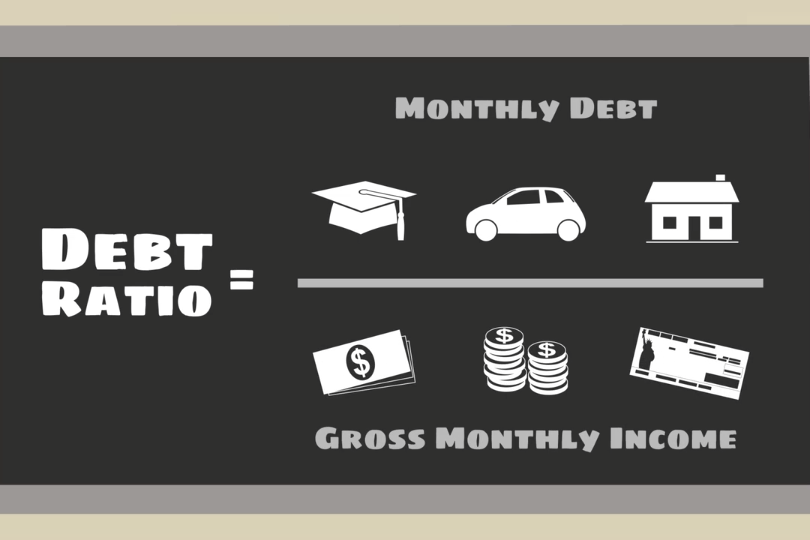

FHA loan debt ratios are financial benchmarks that assess a borrower's ability to manage their debt and make mortgage payments on time. These ratios play a pivotal role in the FHA loan approval process, as they provide a snapshot of a borrower's financial health. Two primary debt ratios are considered when evaluating an applicant's eligibility for an FHA loan:

Front-End Ratio (Housing Ratio)

This measures the percentage of a borrower's monthly gross income that will be allocated to housing-related expenses. These expenses include mortgage principal and interest, property taxes, homeowners insurance, and mortgage insurance premiums (if applicable). FHA guidelines typically require that the housing ratio does not exceed 31% of the borrower's gross income.

Back-End Ratio (Total Debt Ratio)

This is a broader measure of a borrower's debt load. It considers not only housing-related expenses but also other monthly obligations such as car loans, credit card payments, student loans, and any other outstanding debts. The FHA generally sets a maximum allowable back-end ratio of 43% of the borrower's gross income.

To improve your back-end ratio, focus on paying down existing debts, such as credit cards and personal loans. Reducing your overall debt load can make you a more attractive candidate for an FHA loan.

Both of these ratios serve as vital tools for lenders to assess your financial health and determine your eligibility for financing. By managing your debt wisely, increasing your income, and budgeting carefully, you can improve your debt ratios and increase your chances of securing an FHA loan. Remember that while debt ratios are an essential part of the approval process, they are just one piece of the puzzle, and other factors like credit score and down payment also play a role in determining your loan eligibility.

------------------------------

RELATED VIDEOS:

Let's Talk About Home Equity

Understanding Your Loan Term

Your Home Loan is Called a Mortgage

FHA Loan Articles

April 16, 2025There are smart uses for cash-out refinancing loan proceeds and uses for that money that may work against the borrower. We examine some of those choices below, starting with using an FHA cash-out refinance for investment purposes. Is this a good idea?

April 15, 2025House hunters sometimes face a curveball when the appraisal for a home they want to buy with an FHA mortgage is lower than the offer. Is this a deal-breaker? Believe it or not, it isn't the end of the road. A low appraisal can sometimes be just a bump in the road. In other cases, you may wish to walk away from the deal. Here's your game plan to navigate this situation...

April 14, 2025 Buying a home with an FHA loan can be an exciting and achievable goal. This quick quiz helps you gauge your understanding of FHA loans and what it takes to make a winning offer on your new dream home. Take a few moments to answer the questions and see how prepared you are to navigate this crucial stage of your home-buying journey.

March 31, 2025Is 2025 the right year for you to consider an FHA streamline refinance? These mortgages are for those who want a lower interest rate, a lower monthly payment, or to move out of an adjustable-rate mortgage and into a fixed-rate loan. We examine some of the critical features of FHA streamline refinances.

March 27, 2025Did you know there are FHA loans that let house hunters buy multi-family properties such as duplexes and triplexes? FHA rules for these transactions is found in HUD 4000.1, including owner-occupancy, require that one unit serve as the borrower’s primary residence. Some house hunters ask why this rule exists. Some believe the rule serves as a lender risk mitigation strategy.