Frequently Asked Questions About Home Insurance with an FHA Mortgage

May 14, 2025

There are important nuances to these insurance policies to know before you start. What's the difference between insurance against water damage and flood insurance? As we'll explore below, that's just one example of the "hidden" expenses of buying your new home to budget for.

What kinds of insurance do I need when buying a house with an FHA mortgage?

If you purchase a home using an FHA residential real estate mortgage, you will primarily need to have FHA Mortgage Insurance Premium (MIP) and homeowner's insurance. Additionally, depending on your circumstances and the location of your property, you might need other types of insurance for full protection.

The FHA Mortgage Insurance Premium, or MIP, is a type of insurance that protects the lender against financial loss if you, the borrower, default on your loan. It helps make FHA loans available to a wider range of people.

What are the different parts of the FHA MIP?

The FHA MIP has two parts: the Upfront Mortgage Insurance Premium (UFMIP) and the Annual Mortgage Insurance Premium (Annual MIP).

What is the Upfront Mortgage Insurance Premium (UFMIP)?

The UFMIP is a one-time fee that you typically pay when you close on your house. It is usually a percentage of your total loan amount. While you can pay it in cash at closing, it's also common to add it to your loan balance.

What is the Annual Mortgage Insurance Premium (Annual MIP)?

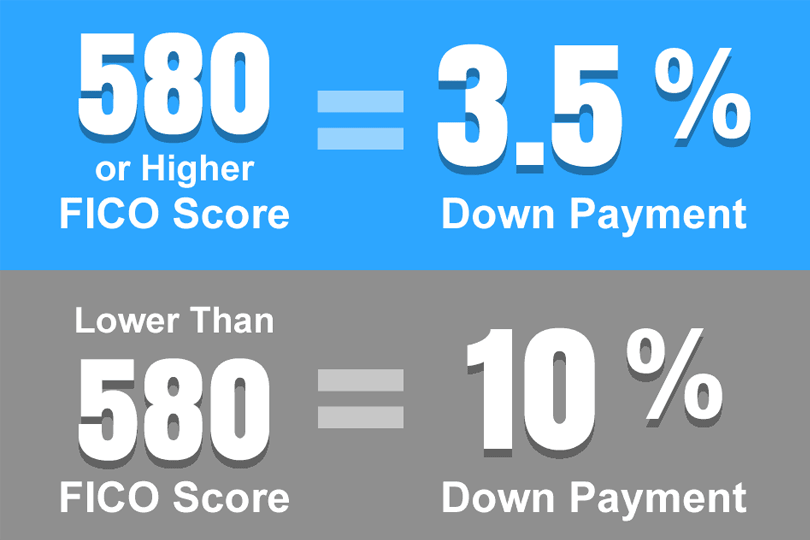

The Annual MIP is an ongoing monthly payment that you make as part of your regular mortgage payment. The amount you pay depends on your loan amount, the length of your loan, and the size of your down payment.

Why do I have to pay the FHA Mortgage Insurance Premium?

The FHA MIP is required because FHA loans are designed to help people who might not qualify for traditional loans, often those with lower down payments or less-than-perfect credit. The MIP reduces the risk for lenders, allowing them to offer these loans.

What is homeowner's insurance (hazard insurance)?

Homeowner's insurance, often called hazard insurance when talking about mortgages, is another type of insurance you must have with an FHA loan. It protects the lender's investment, which is your house itself, from physical damage.

What does a standard homeowner's insurance policy usually cover?

A typical homeowner's insurance policy includes coverage for the structure of your house, other structures on your property, your personal belongings inside the house, additional living expenses if you have to move out temporarily due to a covered loss, liability if someone is injured on your property, and minor medical payments for guests injured on your property.

What kinds of events are typically covered by homeowners' insurance?

Homeowner's insurance usually covers events like fire, windstorms, hail, explosions, riots, damage from aircraft or vehicles, smoke, vandalism, theft, falling objects, the weight of snow or ice, and some types of water damage from things like burst pipes.

Are there things that homeowner's insurance typically doesn't cover?

Yes, most homeowners' policies do not cover earthquakes, floods, landslides, sewer backups (though you can often add this coverage), neglect, pests, and damage from war or nuclear events.

FHA Loan Articles

April 14, 2025 Buying a home with an FHA loan can be an exciting and achievable goal. This quick quiz helps you gauge your understanding of FHA loans and what it takes to make a winning offer on your new dream home. Take a few moments to answer the questions and see how prepared you are to navigate this crucial stage of your home-buying journey.

March 31, 2025Is 2025 the right year for you to consider an FHA streamline refinance? These mortgages are for those who want a lower interest rate, a lower monthly payment, or to move out of an adjustable-rate mortgage and into a fixed-rate loan. We examine some of the critical features of FHA streamline refinances.

March 27, 2025Did you know there are FHA loans that let house hunters buy multi-family properties such as duplexes and triplexes? FHA rules for these transactions is found in HUD 4000.1, including owner-occupancy, require that one unit serve as the borrower’s primary residence. Some house hunters ask why this rule exists. Some believe the rule serves as a lender risk mitigation strategy.

March 25, 2025What does it take to sell a house purchased with an FHA mortgage? Are there special rules, restricrtions, or added considerations? We examine some key questions and their answers to FHA real estate sales issues.

March 24, 2025If you are selling a home, you may need to negotiate with buyers to fund their purchases with an FHA mortgage. What do you, as a seller, need to know about FHA mortgages and how they may differ from conventional loans? We examine some common issues.