Growing Equity Mortgage

Growing Equity Mortgages (GEMs) are part of the FHA’s Section 245(a) loan type that start off with lower initial payments, and increase according to a predetermined schedule over the life of the loan. Similar to a Graduated Payment Mortgage, GEMs are a good option for potential homebuyers who expect higher earnings in the future.

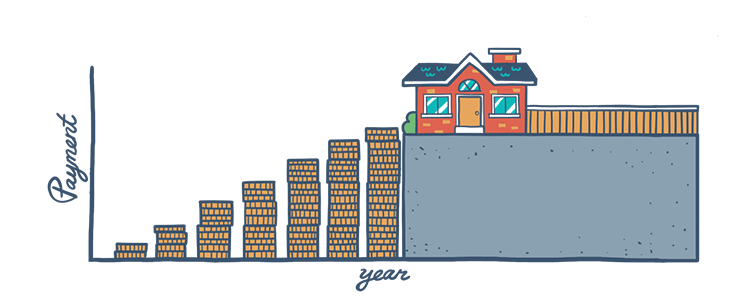

How Does a GEM Work?

Growing Equity Mortgages allow you to purchase a home sooner than you would be able to with most other financing options. There is an introductory year during which your monthly payments are based on a 30-year, fixed-rate schedule. After this initial year ends, your payments increase annually at a fixed rate, depending on the plan that you choose.

The FHA offers five different GEM plans:

- Plan I (Code L):

1% fixed increase per year - Plan II (Code M):

2% fixed increase per year - Plan III (Code N):

3% fixed increase per year - Plan IV (Code O):

4% fixed increase per year - Plan V (Code P):

5% fixed increase per year

GEMs are popular because they can help you own your home sooner. While your introductory payments are calculated based on a 30-year mortgage model, the actual term of your loan is shorter due to the increasing annual payment rate. Your loan term should not exceed 22 years with the lowest plan of a 1% increase, and can be as short as 15 years with the 5% increase.

Every month, more and more money goes towards the principal amount, and the mortgage is paid off faster, which helps you save on interest. So instead of paying interest over 30 years, you'll pay only as long as it takes to pay off the full principal balance, which is a shorter amount of time due to the GEM guidelines.

Who's it For?

Unlike a Graduated Payment Mortgage, a GEM’s scheduled increments of monthly payments result in a shorter loan term and lower cost to the borrower, because it comes without the risk of negative amortization that can lead to an unmanageable balloon payment.

Though HUD’s 245(a) program was designed to assist low-income first-time homebuyers purchase a home sooner than they would be able to with conventional mortgages, it is open to repeat homebuyers as well. They can all take advantage of the FHA’s lenient qualification requirements such as low down payments and credit scores.

Similar to a Graduated Payment Mortgages, this type of home loan is only eligible to purchase single-family properties or condominiums that will serve as the borrower’s primary residence and not an investment property. This loan type is ideal for borrowers who expect to see a rise in their income and want to own a home sooner. However, it is also important that borrowers be completely positive of their future earning potential and job security when deciding to finance their home with a Growing Equity Mortgage.

FHA Loan Articles

November 22, 2023In the last days of November 2023, mortgage loan rates flirted with the 8% range but have since backed away, showing small but continued improvement. What does this mean for house hunters considering their options to become homeowners soon?

November 4, 2023In May 2023, USA Today published some facts and figures about the state of the housing market in America. If you are weighing your options for an FHA mortgage and trying to decide if it’s cheaper to buy or rent, your zip code may have a lot to do with the answers you get.

October 14, 2023FHA loan limits serve as a crucial mechanism to balance financial sustainability, regional variations in housing costs, and the agency's mission to promote homeownership, particularly for those with limited financial resources.

September 25, 2023Mortgage rates are hitting prospective homeowners hard this year and are approaching 8%, a rate that didn't seem very likely last winter. With so many people priced out of the market by the combination of high rates and a dwindling supply of homes.

September 19, 2023The FHA Handbook serves as a crucial resource for mortgage lenders, appraisers, underwriters, and other professionals involved in the origination and servicing of FHA-insured home loans. It outlines the policies and requirements for FHA-insured mortgages.

September 13, 2023FHA rehab loans are a specialized type of mortgage loan offered by the Federal Housing Administration that allows borrowers to finance both the purchase or refinance of a home and the cost of needed repairs.