How Much Do I Need to Put Down on a House

September 20, 2021

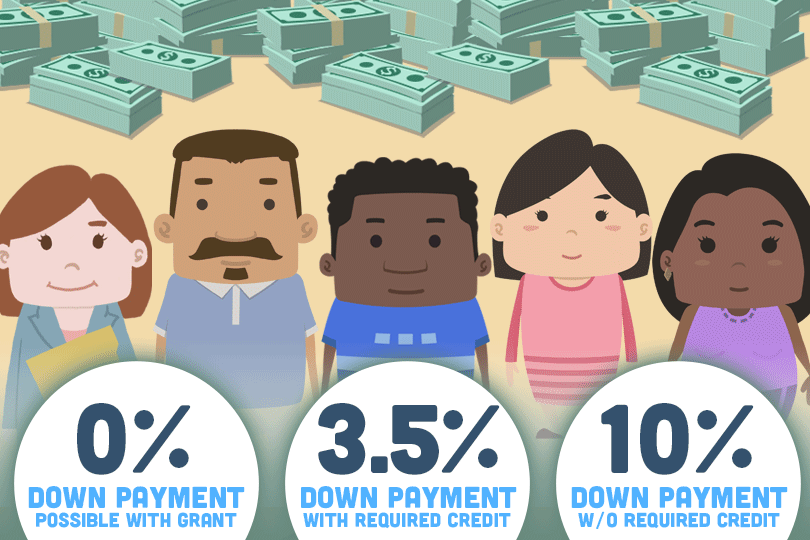

Minimum Down Payment Requirements

Different lenders have different requirements when it comes to the down payment on a home loan.

- FHA loans, backed by the Federal Housing Administration, require only 3.5% down with a 580 credit score.

- VA loans, insured by the U.S. Department of Veterans Affairs, for current and veteran military service members and eligible surviving spouses, have no down payment requirement.

- USDA loans, guaranteed by the U.S. Department of Agriculture's Rural Development Program, do not require a down payment.

- Most conventional loans (those not insured by the government), require a minimum down payment of 20%.

Lenders look favorably on borrowers who are able to make a sizeable down payment, as it gives them peace of mind. FHA-approved lenders feel more secure accepting a smaller down payment since they are insured by the government agency, and the lenders are protected in the case borrowers are unable to pay back the mortgage amount.

Mortgage Insurance

Applying for a conventional mortgage may mean paying for Private Mortgage Insurance (PMI). This is charged to borrowers when they are unable to make the minimum down payment (usually 20%) but still want to apply for it. While this option helps qualify for the loan, it also increases the cost of the loan itself. Borrowers can make a lower down payment upfront, but the monthly PMI premium is added to the mortgage payments. It is also important to remember that PMI does not protect the borrower. Instead, it protects the lender from losses if the borrower defaults on the loan. In most cases, borrowers will only have to pay for PMI until they have amassed enough equity in the home (usually up to the 20% requirement), and can have the premium dropped at that point. Talk to your loan officer to make sure this is an option.

How Down Payments Can Affect Your Interest

The amount of money directly impacts the amount of interest you pay over the life of the loan. Making a larger down payment means paying less in interest, since you are borrowing less money. Imagine that you are buying a $200,000-home with a down payment of $20,000. You will be paying interest on a $180,000 loan. (200,000 – 20,000). However, if you pay only $10,000 upfront, you will be paying interest on a $190,000-loan instead.

Trying to calculate how much money to put down on your home can be daunting, but having the information you need makes the decision easier. It is important that as a potential homebuyer that you do your research and learn about your options, including Down Payment Assistance Programs. Head to www.fha.com to for a comprehensive list of programs for each state.

------------------------------

RELATED VIDEOS:

Do What You Can to Avoid Foreclosure

Homes Financed With FHA Loans Must Be Owner Occupied

FHA Programs for First-Time Homebuyers

FHA Loan Articles

March 25, 2025What does it take to sell a house purchased with an FHA mortgage? Are there special rules, restricrtions, or added considerations? We examine some key questions and their answers to FHA real estate sales issues.

March 24, 2025If you are selling a home, you may need to negotiate with buyers to fund their purchases with an FHA mortgage. What do you, as a seller, need to know about FHA mortgages and how they may differ from conventional loans? We examine some common issues.

March 24, 2025How much do you really know about how FHA home loan interest rates are set and what factors influence them before your lender makes you an offer? We explore some key points about FHA loan rates, FICO scores, and debt ratios.

March 11, 2025Adding a co-borrower to your FHA is a way to offset fears that you won't qualify for the mortgage on your own. An FHA loan co-borrower with a more substantial financial profile may offset the primary borrower's weaknesses, demonstrating a reduced risk to the lender. But for an FHA loan, don't assume that one borrower with good credit scores can offset one with non-qualifying scores. We ask 20 questions about co-borrowing to help you better plan for your FHA loan.

March 10, 2025Even if you aren’t considering your home loan options right this second, it’s smart to know your options if you decide to pursue a new home later. To that end, using a mortgage calculator is a smart choice for setting some basic budgeting parameters as you plan your path toward home ownership. A mortgage calculator helps you plan for future financial scenarios, such as buying new or refinancing a current home.